Discipline

Content design,

content engineering, prompt design

Initiative I led

FBAR content rebuild and

the workflow that scaled it

Partners

PM, PD, Tax Content Analyst,

Corporate Counsel, Eng, Marketing, CX

Surfaces shipped to

FBAR flow, landing page,

error states, success state

The brief

FBAR compliance is genuinely complex, the consequences of mistakes are severe, and the existing copy read like it was written by lawyers for lawyers. The work was to make the flow legible to the people who had to file it, while keeping every legally immovable term intact.

The diagnosis

The existing FBAR content lifted regulatory language almost verbatim from FinCEN documentation. Reading level was college-graduate or higher. Terms like "financial interest," "signature authority," and "owner of record" appeared without plain-language definitions, and passive constructions hid who needed to do what. Users with legitimate foreign accounts were abandoning the flow because they couldn't tell whether they were even required to file.

Why it mattered

FBAR is a high-stakes compliance flow. Filing wrong has real consequences. The audience is unusually wide, ranging from experienced investors to first-time filers who didn't know they were required to file at all. Copy that confused either group sent them somewhere that wasn't TurboTax, which left filers exposed and the product carrying the gap.

What I did

I built a five-phase content engineering workflow on top of Writer.ai that combined prompt engineering with structured legal review. I documented three content principles, a four-point quality checklist, a prompt library, and a decision log so other writers could repeat the process. The workflow let me rewrite the FBAR flow line by line at college-grade level down to eighth-grade level, with every legally immovable term preserved.

The work

Five phases. Three principles. Every rewrite cleared legal.

Five chapters: how the existing copy was failing, the operating model that made the rewrite possible, the discovery that anchored it, the workflow itself, and the screens and rewrites it produced.

Chapter 01

The law was written for regulators. The product was written for no one.

FBAR exists because US persons with foreign financial accounts over $10,000 must report them annually to FinCEN. The legal definitions are precise, the consequences of mistakes are severe, and the audience ranges from experienced investors to first-time filers who had no idea they were even required to file. The existing TurboTax FBAR content read the way it was written, by lawyers and for lawyers, which left a gap between accuracy and usability that the product had no way to close.

The content was accurate, compliant, and unusable. For users trying to file correctly, only clarity resolved the choice between filing right and giving up.

Chapter 02

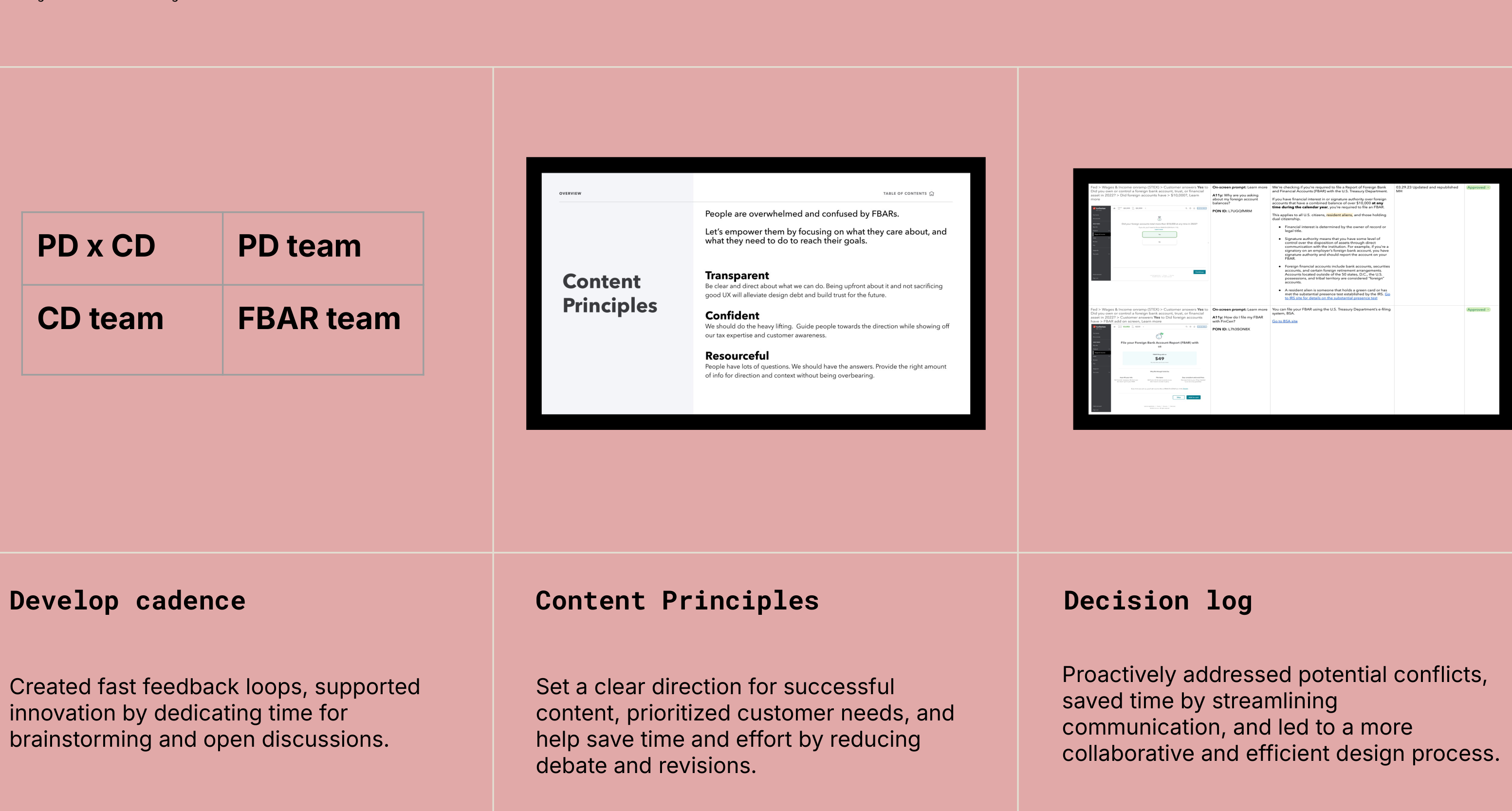

Here's how I planned the work, the timeline, and the cross-functional cadence.

Before writing a single word, I built the operating infrastructure. The FBAR project required unusually close collaboration across product design, legal, tax content analysts, and engineering. I established a structured cadence with the product design team that created fast feedback loops and dedicated time for open discussion. I set content principles early so every stakeholder shared a direction before any copy existed. And I built a decision log that proactively documented every content call and its rationale, which reduced back-and-forth and gave legal a record they could reference instead of relitigating decisions.

The content principles I established for FBAR were grounded in three ideas. Transparent meant being clear and direct about what TurboTax could do and where it stopped, building trust through honesty. Confident meant guiding users toward the right direction while showing tax expertise and customer awareness. Resourceful meant providing the right information without being overbearing. Every piece of copy passed through that filter before it went to legal.

Chapter 03

I started with discovery and research.

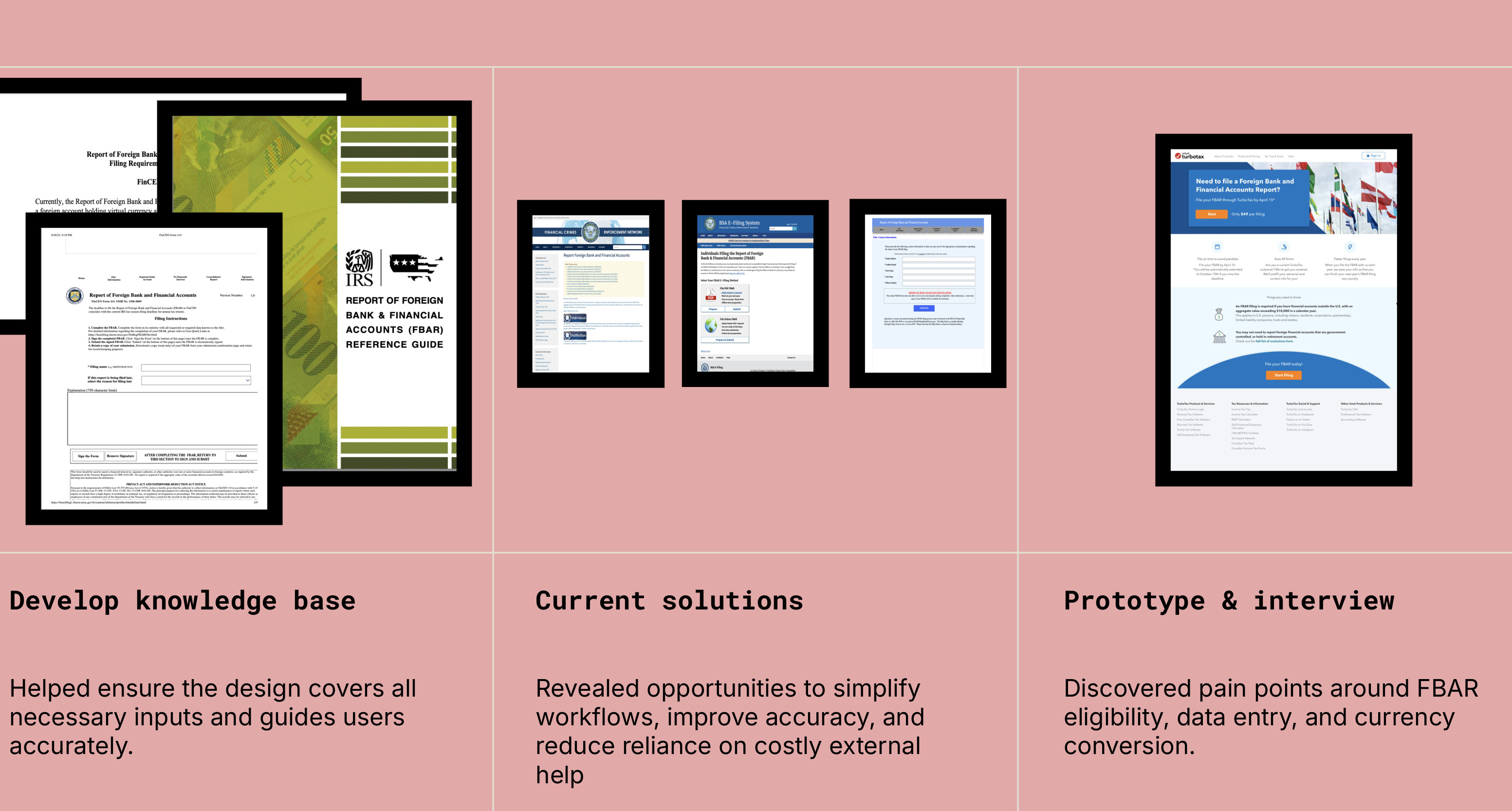

I studied FBAR regulations through primary documentation and SME interviews, dissected existing solutions including the FinCEN BSA e-filing system and external FBAR services, and conducted user interviews and prototype testing. One filer in the interviews paused on the qualification screen, read it three times, and said "I don't know if this is asking me a question or telling me a rule." That was the pattern. The research uncovered three consistent pain points: confusion about FBAR eligibility, difficulty with data entry especially around currency conversion, and anxiety about whether they had filed correctly. FBAR caused anxiety, frustration, and confusion at proportions that went well beyond a typical tax flow.

User research surfaced what people needed at each moment in the flow: reminders and clear tracking, confidence that they had filed correctly, saved bank account information for returning users, and specific currency conversion guidance. None of those needs were being met by the existing content, which is what made the rewrite scope addressable through copy rather than only through new features.

Chapter 04

I built a content engineering workflow on Writer.ai.

The core challenge was scale. Dozens of screens, each with legally specific language that couldn't be rewritten casually. Manual rewrites one by one would take months and introduce inconsistency. I built a five-phase workflow on top of Writer.ai with prompt engineering as the engine and human judgment at every decision point that mattered.

01

Analysis and discovery: map every pain point before touching copy.

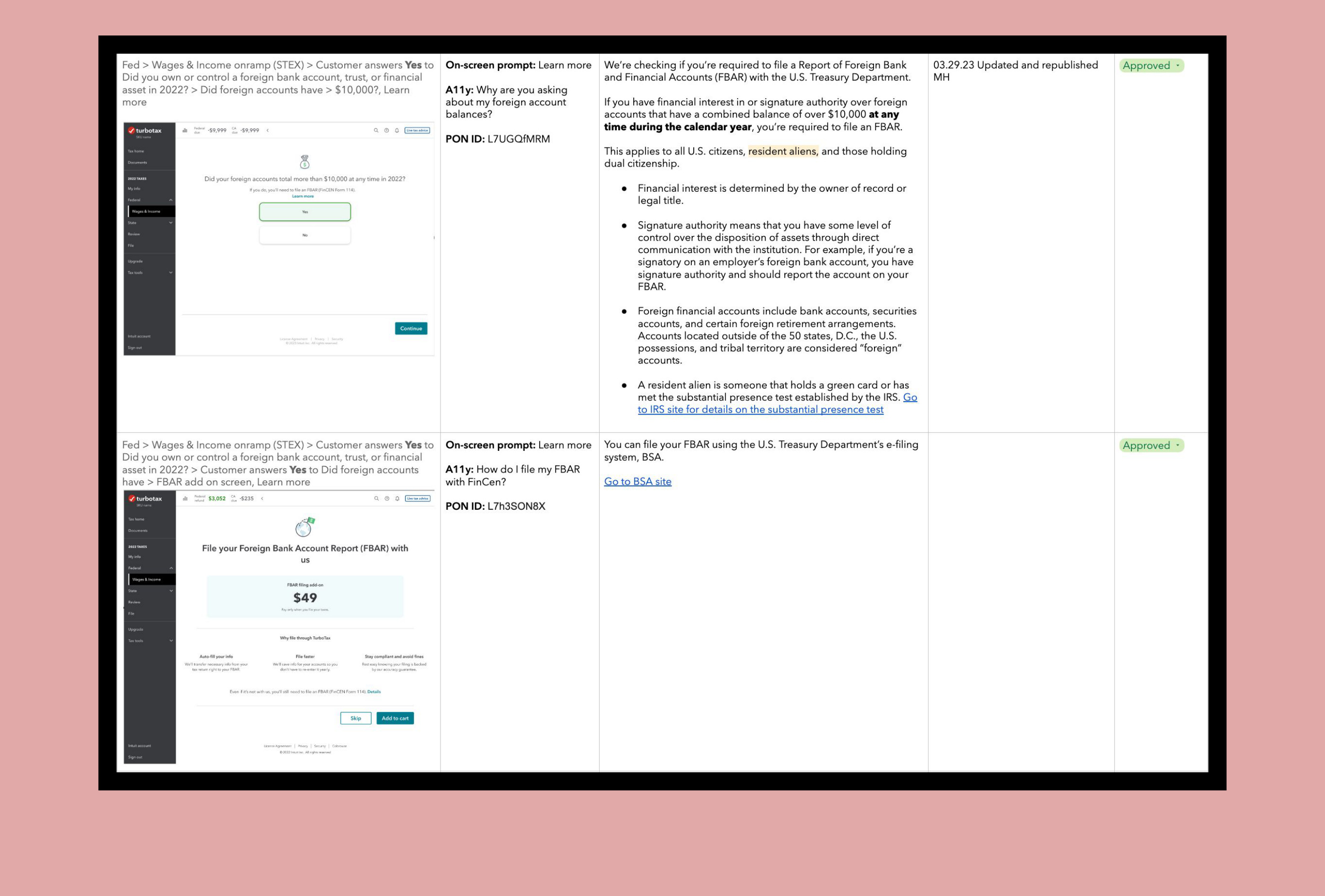

I reviewed the existing FBAR experience and documented every term that confused users in research, every complex explanation around filing requirements, and every recurring pattern from CX call logs. This audit became the brief for the prompt engineering phase that followed.

02

Prompt construction: encode the constraints before touching the copy.

Each prompt included the original text, the legally immovable terms, the target reading level (eighth grade), the voice directive (active, direct address), and the specific question a user is trying to answer at this moment in the flow. The prompt was a specification for a particular content decision rather than a generic "simplify this" instruction.

03

Output evaluation: a four-point quality check before anything left my desk.

Every AI-generated rewrite passed four checks: accuracy (no meaning change), compliance (required terms preserved), readability (measurably lower reading level), and voice (active, direct, second person). Anything that failed any check was revised manually or reprompted.

04

Legal review: structured evidence, not just rewrites.

Each submission to legal included the original, the rewrite, a side-by-side term comparison showing every immovable term was preserved, and a readability score delta. Legal could review for compliance without having to also evaluate clarity, because the two concerns were separated by design.

05

Documentation: prompt library and decision log for team transfer.

Every approved rewrite and its prompt went into a shared library, and every legal decision went into the decision log. I led workshops to teach the prompt engineering approach to the broader content team, and I built a decision framework for when to use GenAI versus traditional development. The second round of FBAR updates took a fraction of the time the first round had.

What the prompts looked like.

Prompt example · financial interest definition

Simplify the following FBAR content while maintaining technical accuracy.

Constraints:

Preserve exactly: "financial interest," "owner of record," "legal title"

Target: eighth-grade reading level

Voice: active voice, direct address ("You have a financial interest when...")

Max sentence length: 20 words

User context: This person is trying to figure out whether they need to report a foreign account. They are not a tax professional. They may be anxious about whether they have done something wrong.

Original:

"Financial interest is determined by the owner of record or legal title. The FBAR regulations provide that a United States person has a financial interest in a foreign financial account for which the United States person is the owner of record or has legal title, whether the account is maintained for his own benefit or for the benefit of others."

Chapter 05

Here's the redesigned experience, screen by screen.

The work shows up in the screens. Every content decision was annotated with its purpose, hierarchy, and tone so the design team and engineering shared the same context. The content notes were a structured part of the design artifact rather than informal Figma comments, which is what kept the intent intact through to engineering.

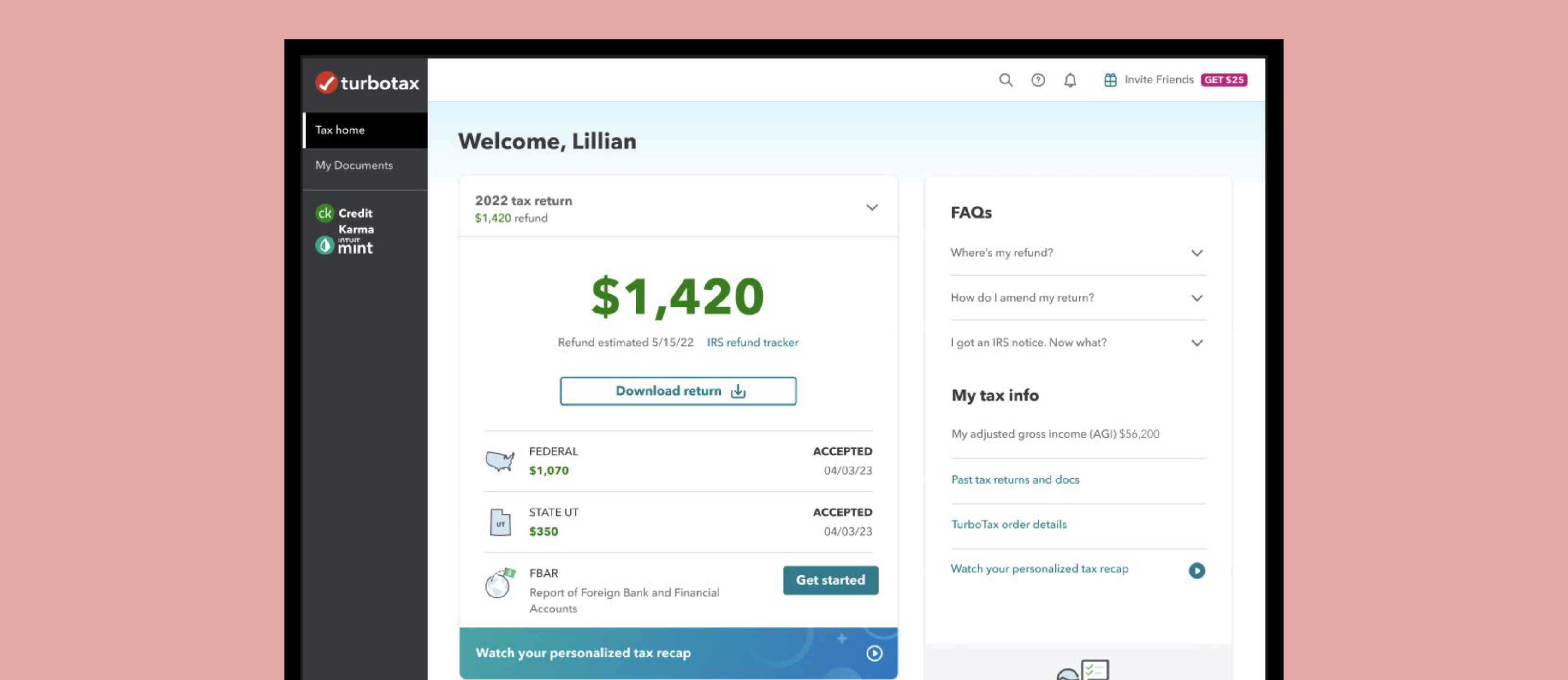

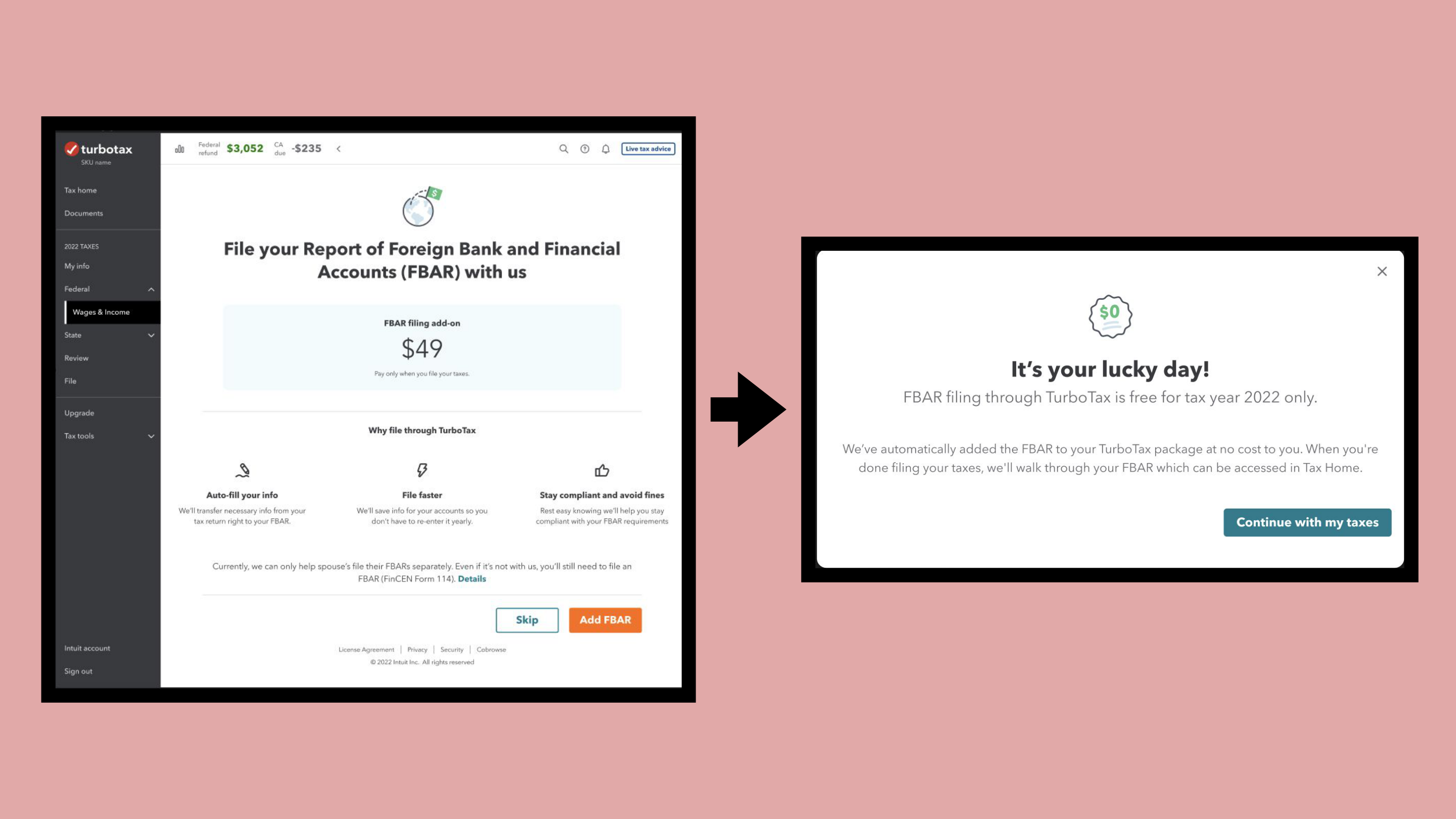

The entry point from the main tax flow.

FBAR begins on the post-filing dashboard, alongside the federal and state returns the customer just submitted. The FBAR row is treated as a peer to the rest of the return, with a clear Get started CTA. Surfacing it here lets a Premier filer discover the obligation while they are still in the act of finishing their taxes, instead of finding out months later from a notice.

Before and after: the flow entry.

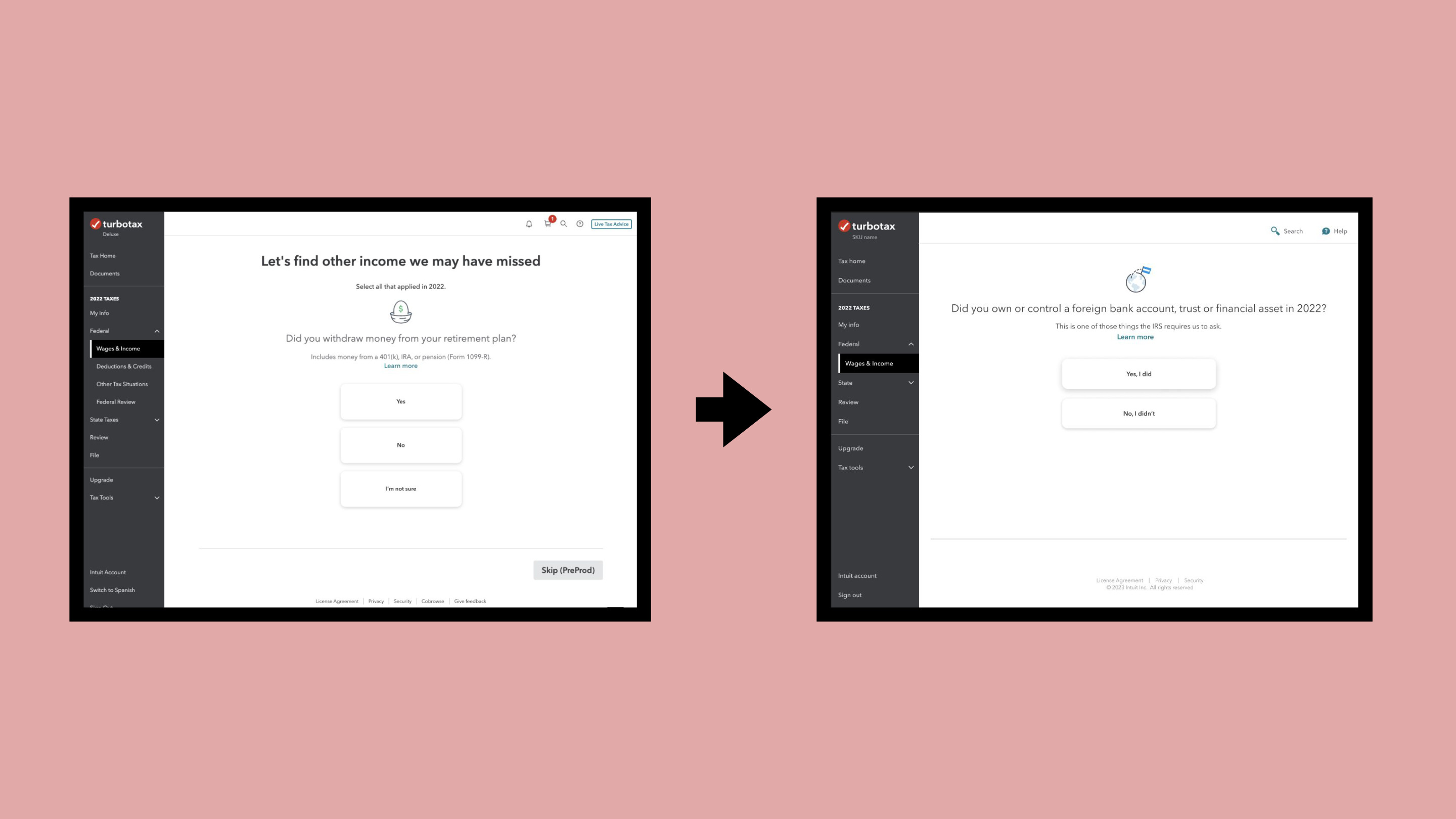

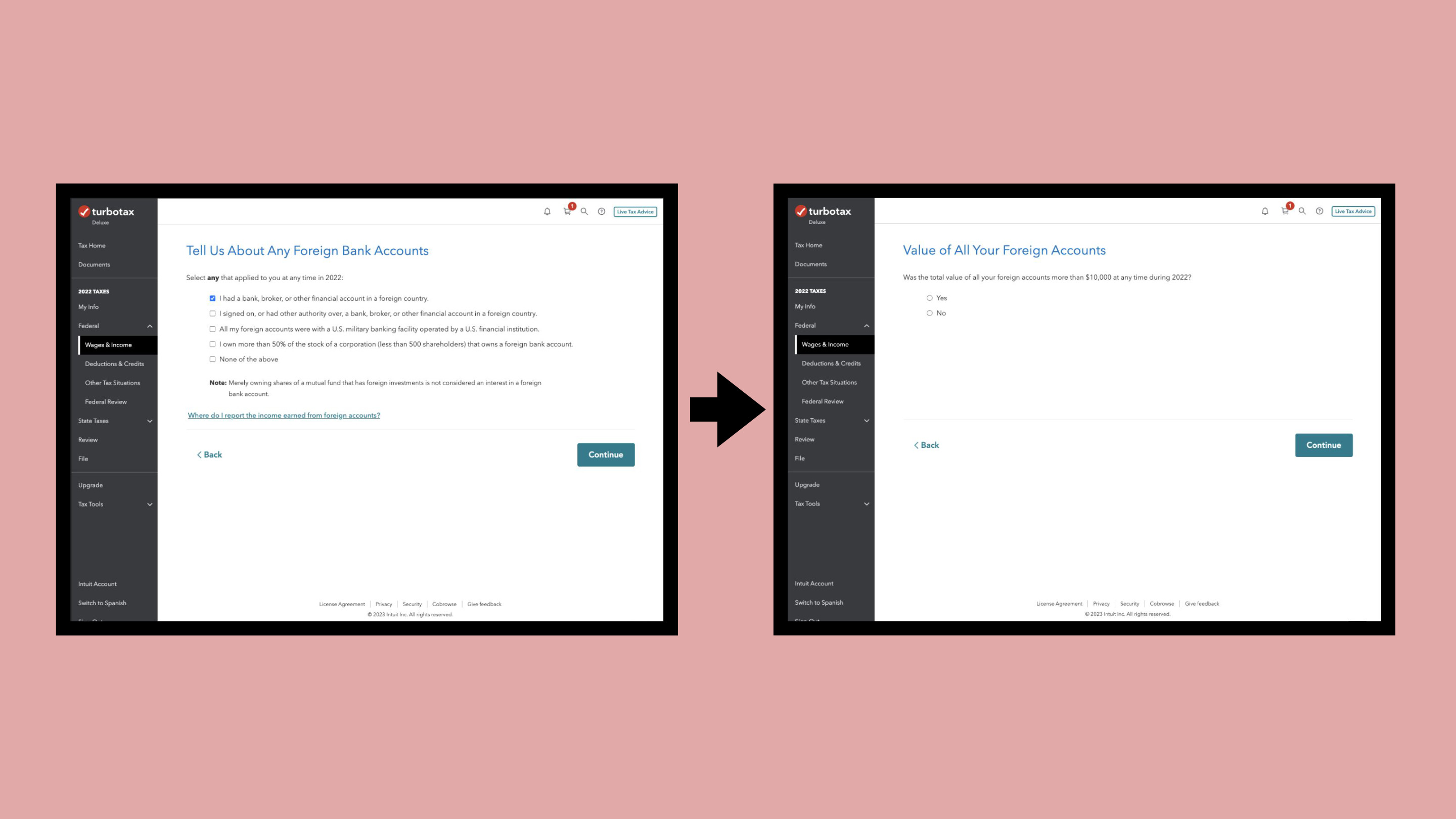

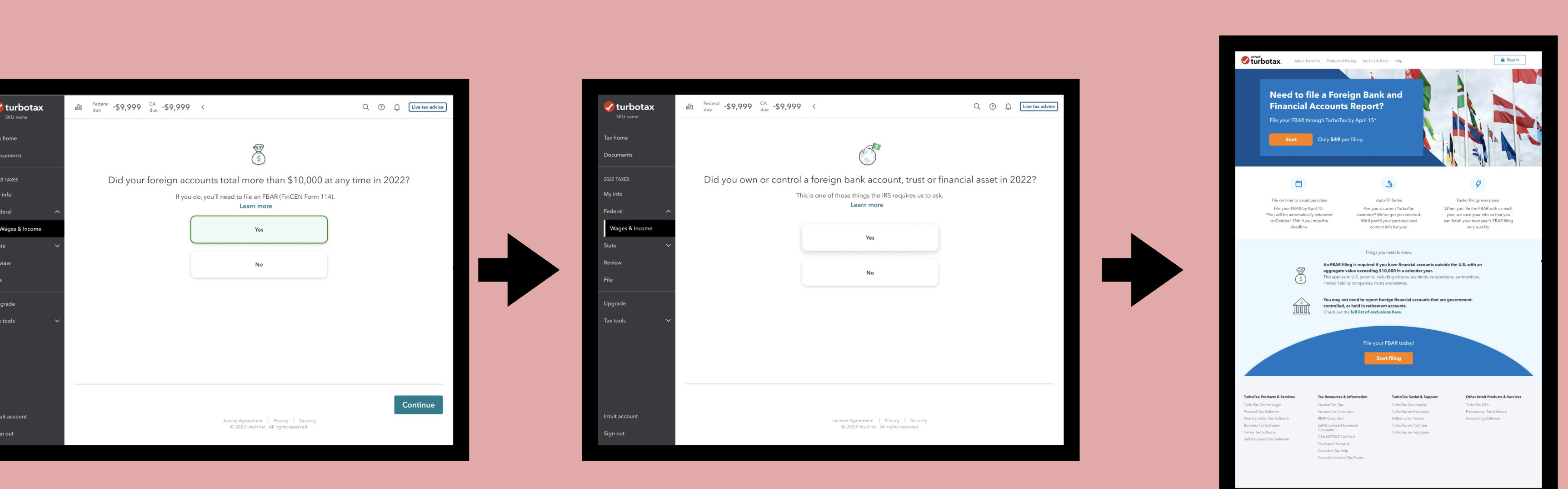

The qualification flow.

Three screens carry the qualification logic: the dollar-threshold check, the ownership-or-control confirmation, and the marketing landing page that catches anyone who arrives outside the flow. Every step states the IRS requirement and lets the filer self-identify in their own words, instead of asking them to interpret regulatory language.

The landing page: before and after.

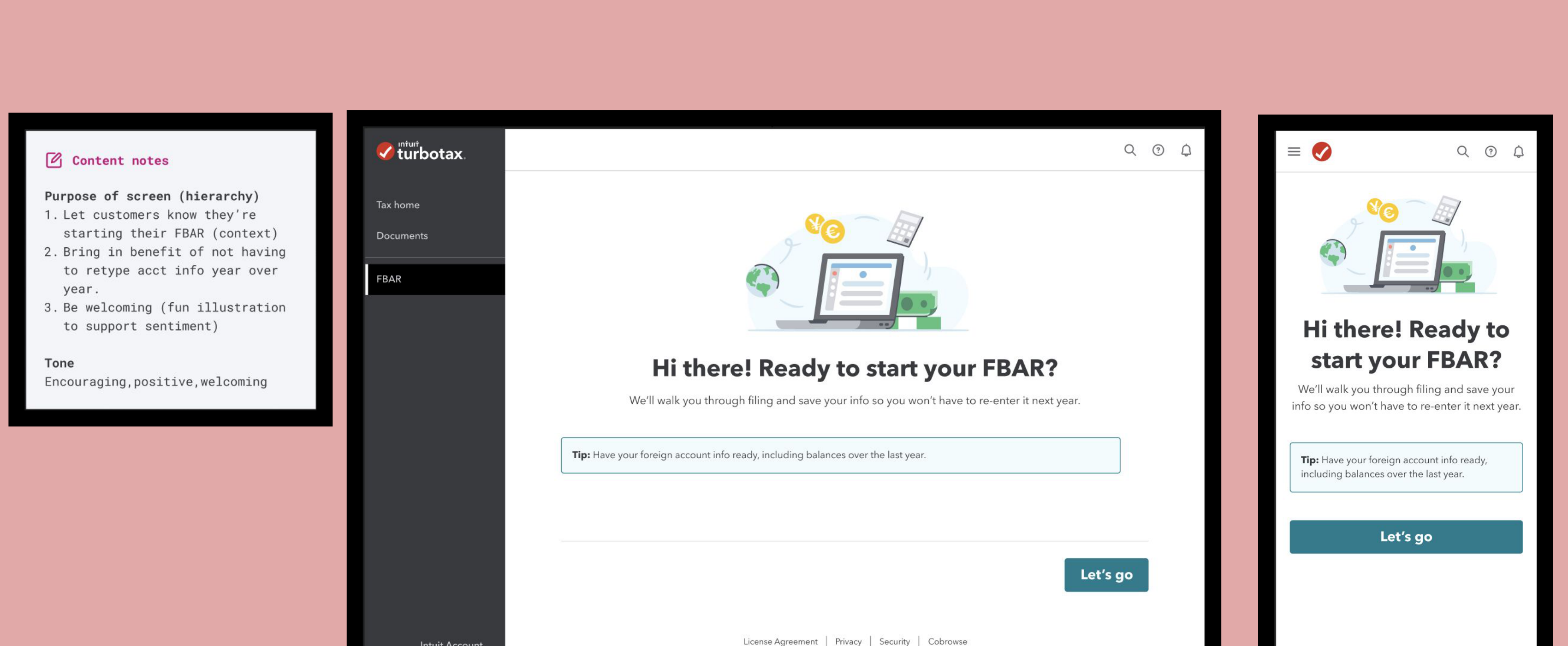

Content notes in context.

Every key screen shipped with annotated content notes that documented the purpose hierarchy and the tone. These were a structured part of the handoff artifact and ensured engineering understood the intent behind every word.

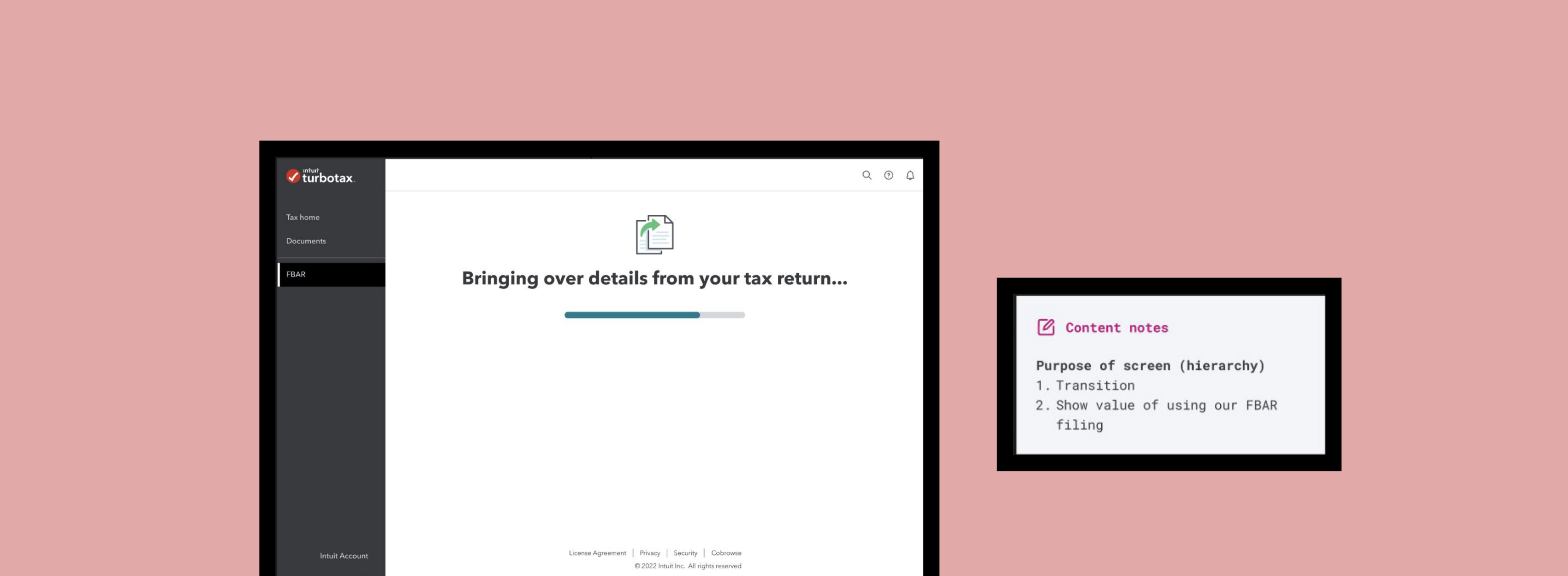

Even the lightest screens carried notes. The data-transfer transition reads as a moment of trust: the system is doing work the filer would otherwise have to redo by hand. The note documents both jobs the screen has to do, so engineering and motion design ship the same intent.

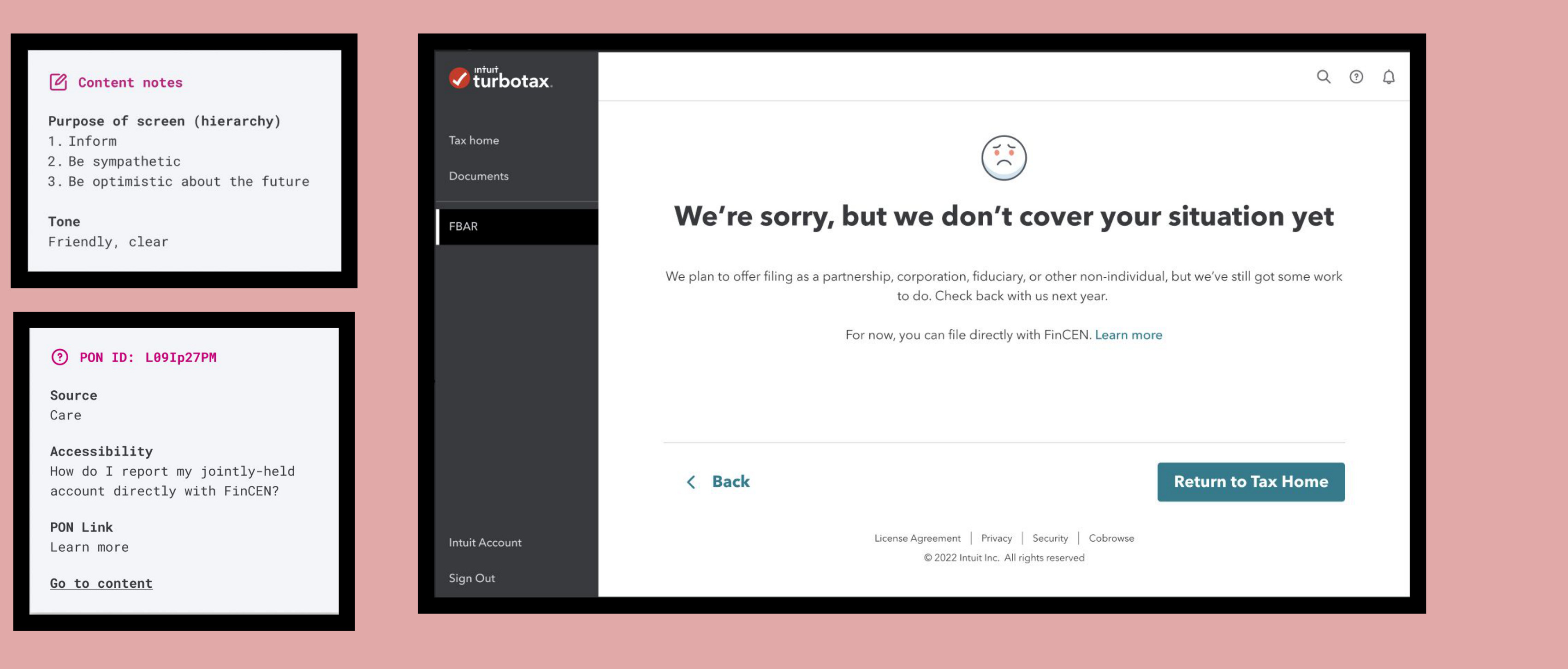

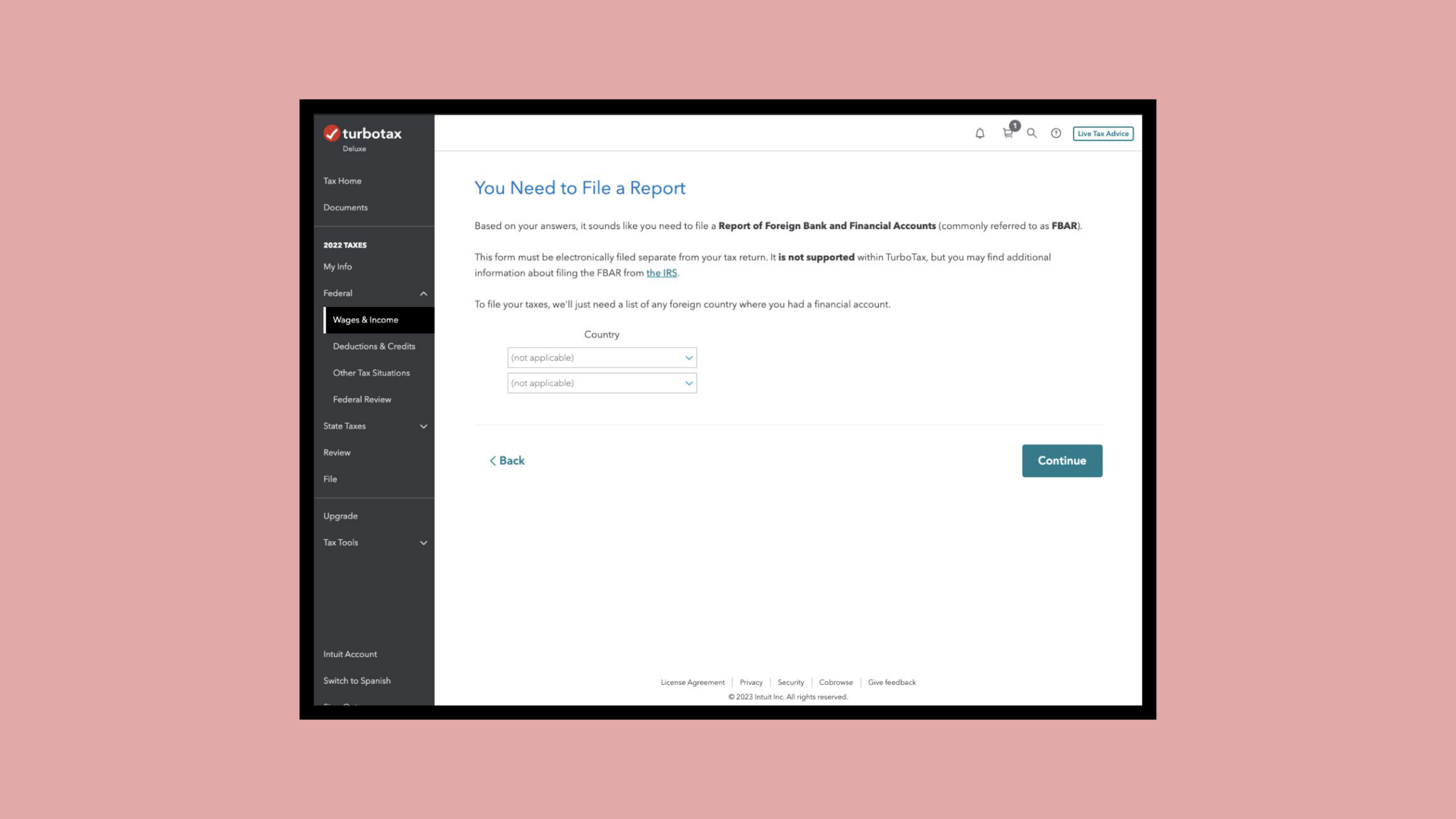

The "You Need to File a Report" screen required particular care. TurboTax couldn't file the FBAR directly at the time, and that constraint had to be communicated honestly without causing panic or breaking trust. Empathetic honesty at a high-stakes moment is one of the hardest content problems in compliance work, and the screen had to lead with what was true and actionable instead of with an apology.

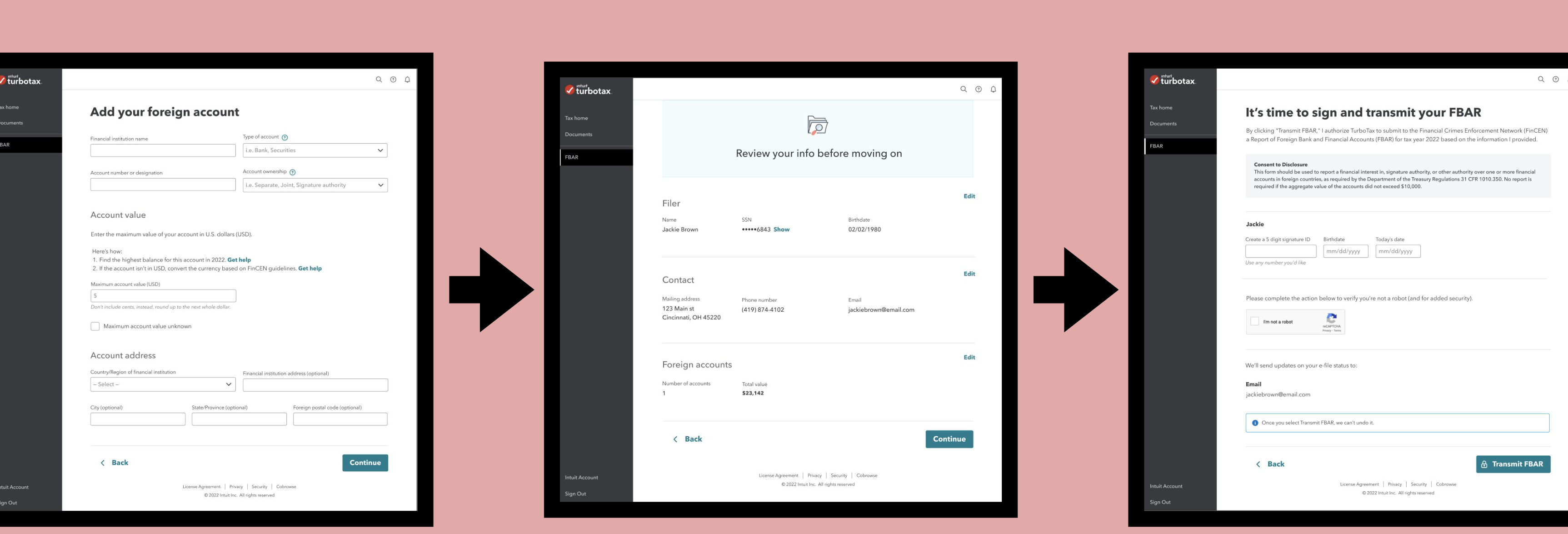

The filing flow itself.

Three screens carry the actual filing: account entry, review, and sign-and-transmit. Each one keeps the legally immovable terms (FinCEN, Consent to Disclosure, Transmit FBAR) verbatim while letting everything around them speak in plain language. The Review step exists because the rewrite made the data feel light enough to lose track of, so the screen pauses the filer before transmission and shows the inputs in groups they can scan in a single read.

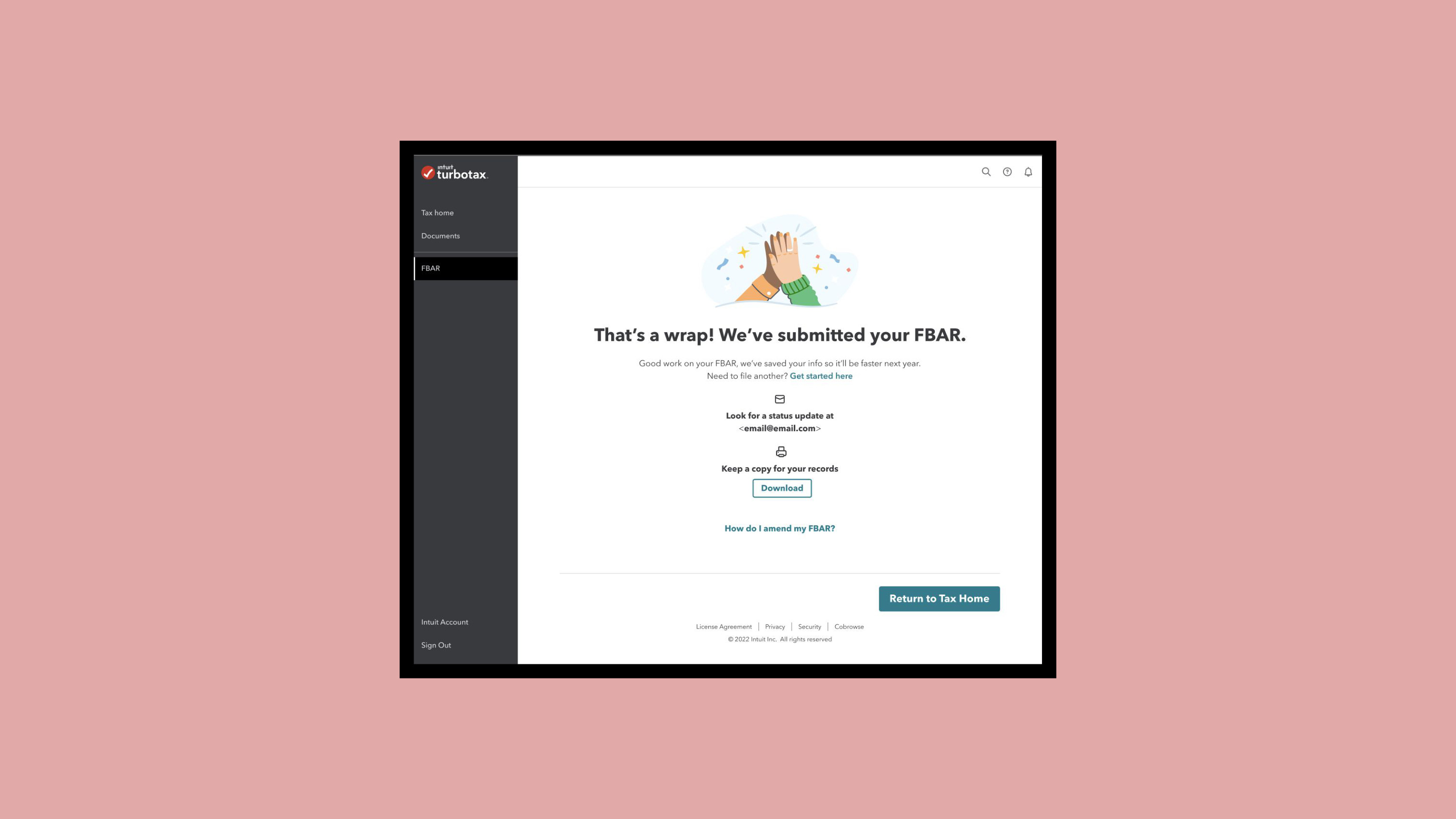

The success state.

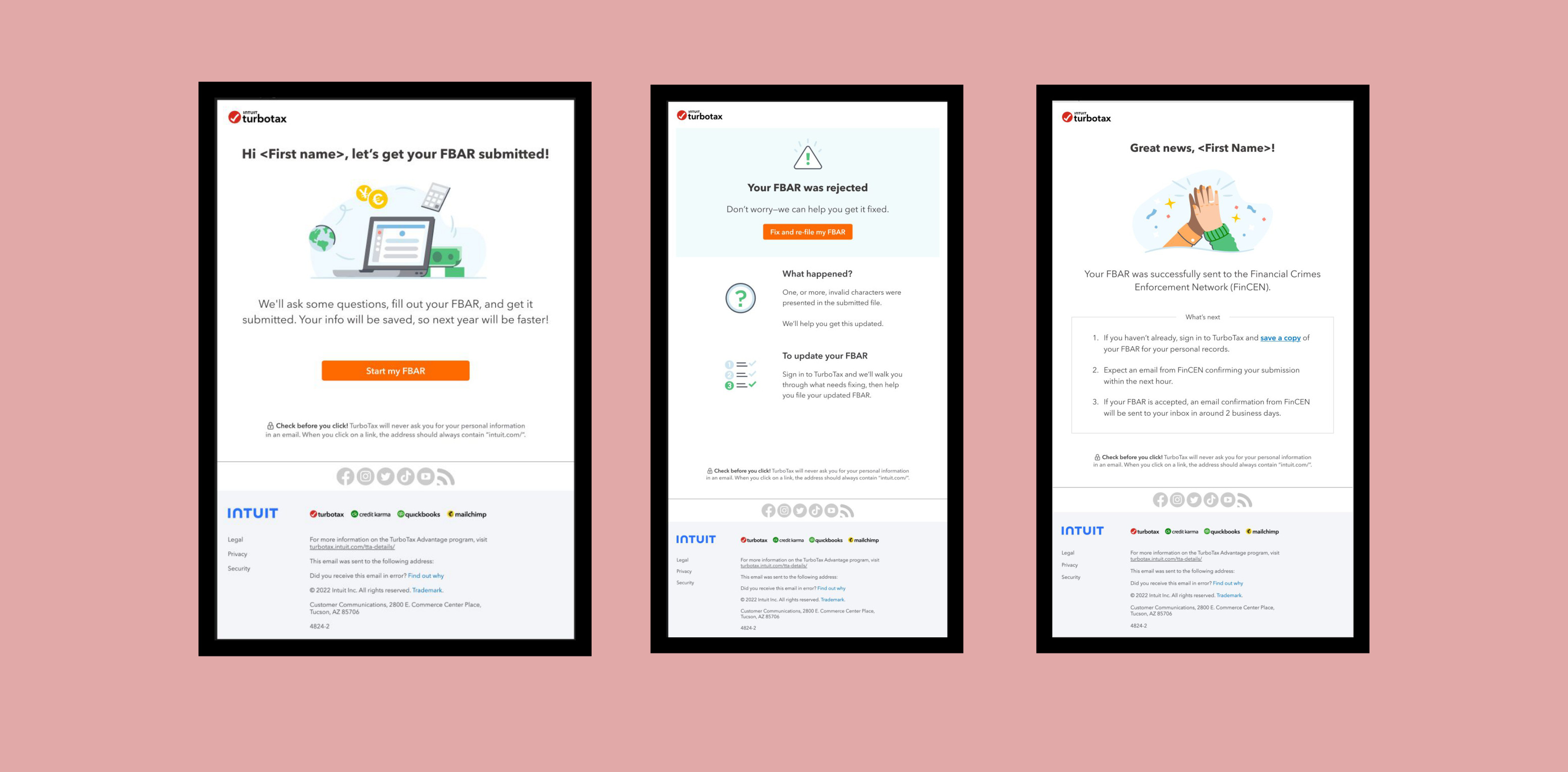

Beyond the product: the email layer.

FBAR doesn't end at the success screen. Three email moments carry the rest of the relationship: a pre-filing nudge that frames the work ahead, a rejection note that holds trust when something goes wrong, and a confirmation that closes the loop with the IRS. Each one follows the same content principles as the in-product flow, so a filer hears one voice across product, email, and support.

Chapter 06

Three rewrites show the workflow at the line level.

Each rewrite preserved every required legal term while cutting reading level, eliminating passive voice, and reorienting the copy around the question a user was trying to answer. The output was copy that helped someone make a correct decision instead of copy that demonstrated regulatory expertise.

Before

"Financial interest is determined by the owner of record or legal title. The FBAR regulations provide that a United States person has a financial interest in a foreign financial account for which the United States person is the owner of record or has legal title, whether the account is maintained for his own benefit or for the benefit of others."

Reading level: college graduate. Passive voice. No direct address. User cannot determine if this applies to them.

After

"You have a financial interest in a foreign account when you're the owner of record or hold legal title to it, even if you hold it for someone else's benefit."

Reading level: eighth grade. Active voice. Direct address. User knows immediately whether this applies to their situation.

Before

"A United States person has signature authority over a foreign financial account if the United States person can control the disposition of money, funds or other assets held in a financial account by direct communication (whether in writing or otherwise) to the bank or other financial institution where the financial account is maintained."

84 words. Two-clause sentence. No example. User must decode what "direct communication" means for their employer's account.

After

"Signature authority means that you have some level of control over the disposition of assets through direct communication with the institution. For example, if you're a signatory on an employer's foreign bank account, you have signature authority and should report the account on your FBAR."

Concrete example included. The employer scenario, the most common confusion point, is addressed directly.

Before

"Did your foreign accounts total more than $10,000 at any time in 2022? If you do, you'll need to file an FBAR (FinCEN Form 114)."

Threshold buried after the condition. "You'll need to" uses future tense and creates uncertainty. No context for what "at any time" means in practice.

After

"Did you own or control a foreign bank account, trust, or financial asset in 2022? This is one of those things the IRS requires us to ask."

Reframed as a straightforward question. The IRS framing removes anxiety by normalizing the question and clarifying TurboTax is asking on behalf of the requirement.

Three signals confirmed the system had taken hold:

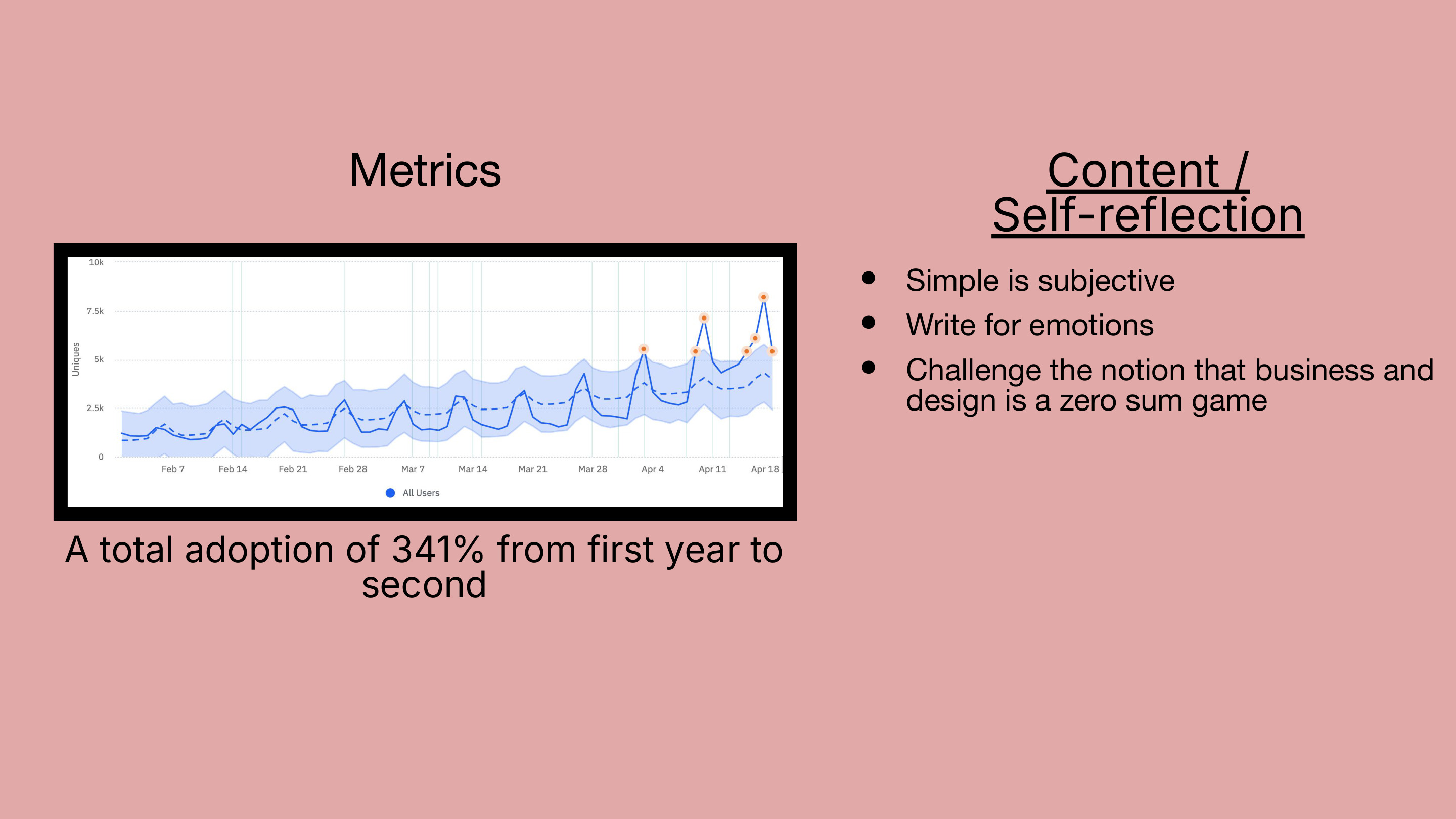

- Year-over-year adoption increased 341%. The flow structure was unchanged, and the only thing that changed was the content, which means users who had previously abandoned because they couldn't determine whether they qualified now completed the flow.

- Time-to-complete dropped 24%. Users who had been re-reading paragraphs to extract a yes-or-no qualification answer started finishing the flow on a single pass, because once the language stopped fighting them, the friction the experience had inherited from FinCEN documentation went with it.

- Premier-tier filer retention rose 19% year-over-year. FBAR is a Premier-SKU feature and the flow had been the leakiest entry point in the segment, so filers who finished the rewritten flow were measurably more likely to return the following year, turning a compliance liability into a retention surface for one of TurboTax's higher-margin tiers.

Read together, the three numbers tell a single story. More people started the flow because the entry point finally explained who it was for. More people finished it because the language stopped extracting tax law from them and started answering their question. More of those people came back the following year because the experience graduated from regulatory ordeal to a routine part of filing. The downstream business effect was Premier retention, and that was the part that turned a content rewrite from a UX win into a revenue argument the next time legal-language friction came up on the roadmap.

Note on metrics. FBAR adoption, time-to-complete, and Premier-tier retention are Intuit-internal year-over-year reads on the FBAR-flow cohort. The flow structure was unchanged in the release; the rewrite was the only major copy intervention, which is the cleanest content-attribution claim available. Specific cohort sizing and confidence intervals are subject to NDA.

Reflection

Here's why this matters now.

The transferable problem

Every product that operates under legal or regulatory constraints faces a version of this problem. The language that satisfies compliance teams is rarely the language that helps users, and most teams resolve that tension by defaulting to compliance, leaving accuracy intact and clarity to whoever can figure it out.

What the FBAR work produced was a way to resolve that tension systematically. A workflow that gave legal teams the evidence they needed to approve plain-language rewrites, a repeatable process for producing them, and a content standard that could survive team turnover. The 341% adoption lift is the headline. The workflow is the part that ports to the next regulated flow.

Up next

Issue №03

Abandonment to adoption.

→